As a second-wave of lockdowns are implemented in many countries around the world, small retailers continue to suffer financially from the extended pain of Coronavirus. But people still need to shop – both for the essentials like food and toilet paper (what goes in, must come out…) and also for the small luxuries and diversions that help preserve a bit of mental sanity while everyone is stuck kicking their heels at home.

Although it’s damaged their brick-and-mortar counterparts, the Coronacomony has proven to be a huge tailwind for the online retail giants, in particular Amazon.

With that backdrop in-mind, Albert and I used this week’s Telescope Investing podcast episode to take a deeper look at the megatrend of e-commerce and online retail, deep-diving into a couple of Amazon’s competitors, both domestically in their home market of the US, and internationally in South East Asia, Africa, and Latin America.

You can listen to the full episode here, but with one of the stocks we reviewed, MercadoLibre (MELI), reporting blow-out earnings last night, I thought I’d share a quick written recap on the company, and their latest earnings report.

I currently have a 5% stake in MELI which I’m considering adding to, so this article is primarily intended as a summary for my own benefit – and per the usual disclaimer, it’s not a recommendation to act, and you need to take your own financial decisions.

Background

MercadoLibre means “free-market” in Spanish. The company is the number one e-commerce player in the eighteen Latin America markets in which it operates (Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, Mexico, Spain, Ecuador, Guatemala, Honduras, Peru, Panama, Uruguay, and Venezuela), also facilitating cross-border trade across LATAM.

MELI offer a number of cohesive services to their customers:

- Mercado Libre Marketplace – an online marketplace connecting buyers and sellers for fixed-price and online auctions, think Amazon + eBay

- Mercado Envios – logistics and delivery, think Fedex (or Amazon again!)

- Mercado Pago – payments and banking platform including mobile point of sale, think PayPal + Square

- Mercado Publicado – providing branding and marketing solutions

- Mercado Credito – providing credit lines for buyers and sellers

The company is headquartered in Buenos Aires, Argentina, and was founded in 1999 by Marcos Galperin, Hernan Kazah and Stelleo Tolda. Hernan Kazah left in 2011, but Marcos Galperin remains the chairman, president and CEO, and Stelleo Tolda acts as President and Chief Operating Officer.

Insiders collectively own 12% of the company today, and MELI has a 4.4 (out of 5) rating on GlassDoor, with Marcos Galperin holding a 96% CEO approval rating.

MELI IPO’d in August 2007 with a market cap of $800M and was the first LATAM tech company listed on the NASDAQ. After the release of Q3 earnings last night, the stock opened today with a market cap of $98B, a 120x gain since going public.

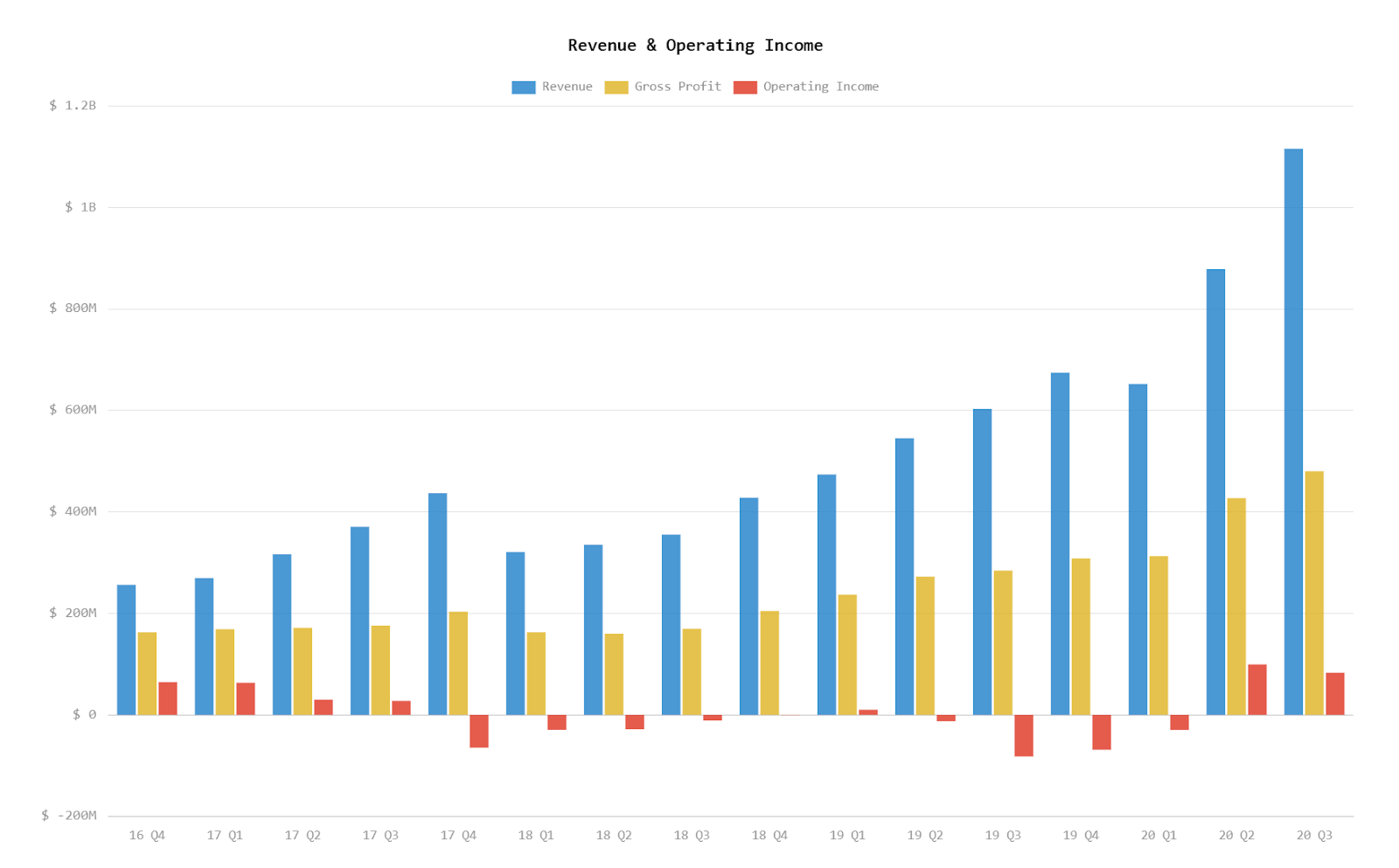

2020 Q3 earnings

The headline figures in last nights’ results were revenues, which have more than doubled in each of the company’s largest markets (all figures in local currency) – Brazil (+112%), Argentina (+260%), and Mexico (+140%). Overall, revenue was up 85% year over year in US dollars – equivalent to 149% in local currencies. This is quite frankly astounding growth, and way ahead of market expectations.

Unique active users have also grown by 92% to 76 million, and the company has sold 206 million items, up 110% year-over-year.

Mercado Envios was able to ship 187 million items during the quarter without any significant disruptions, representing a 131% year-over-year increase.

The total payment volume through Mercado Pago reached $14.5 billion, a year-over-year increase of 92% in USD (161% in local currency). Total payment transactions increased 146% year-over-year, and MELI faciliated nearly 560 million transactions for the quarter.

The company has been investing hard internally, and so while revenues are up across almost all parts of the business, gross profits were $480.2 million with a lower margin of 43.0%, compared to 47.2% in the third quarter last year. Although the company are spending more on R&D and sales & marketing, the primary reason for this drop was quoted as “resulting from an increase in shipping operating costs as we opened new centres”. A similar comment was made in the Q2 earnings call, so this remains a consistent impact for 2020.

What for the future?

It’s impossible to predict exactly what the future will hold for MercadoLibre, but they measure up strongly against many of the lenses that we use to assess companies at Telescope Investing.

There are 656 million people living in Latin America, over two-thirds of whom have a mobile phone. In 2019, across the whole of Latin America, retail e-commerce sales were estimated at being over $80 billion. Even after last night’s reported growth, MELI currently still only capture a tiny fraction of their total addressable market, and the company has huge room for future growth as they increase their market share of this digitally-connected customer base in one of the fastest-growing e-commerce markets in the world.

As with any early-stage growth investment, there are risks. Chief amongst these for MELI I would assess as being the potential of future competition from Amazon, who launched in Brazil in 2019. However MercadoLibre has a long head start, and they have a leadership team who really understand the Latin American market; personally, I think they’ll do just fine.

I opened my first position in MELI in August 2019 (at $623), and added to this in July 2020 (at $1018). At today’s price of $1,440 the stock is currently trading at a rich 25x price to sales ratio, but despite this, I now feel ready to increase my holding. Per my preferred approach of ‘buying in thirds’ and ‘adding to your winners’, I’ll be looking for an opportunity to increase my current 5% stake over the coming weeks, perhaps if the anticipated volatility of the US elections puts a number of my growth stocks on sale at bargain prices.

And just to close, a reminder of that disclaimer – this is not a recommendation to act, and you need to take your own financial decisions!

Looks interesting thanks